Picking the wrong construction contract is like booking a flight without checking where it lands. You think you are going somewhere good. Then reality hits. Disputes start. Costs spike. Deadlines get missed. The choice you made before the first brick was laid ends up defining the entire project.

This guide explains the most common construction contract types, Lump Sum vs Item Rate vs Cost Plus Contracts, in plain language. No complicated legal terms. Just clear, practical information.

Key Takeaways:

- A lump sum contract sets one fixed total price. The contractor carries the financial risk, not the owner.

- An item rate contract pays the contractor per unit of work based on actual quantities measured on site.

- A cost-plus contract reimburses all real project costs plus an agreed fee for the contractor’s profit.

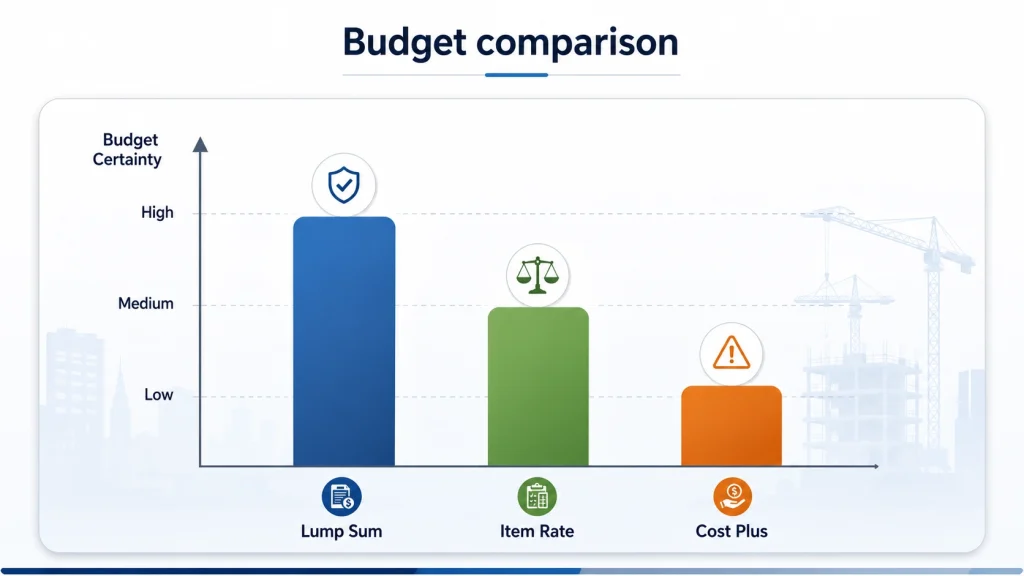

- A lump sum gives the owner the highest cost certainty. Cost plus gives the least.

- Item rate contracts are the standard choice for government and public sector infrastructure projects.

- The owner carries almost all financial risk in a cost-plus contract. A GMP clause can limit that exposure.

- A lump sum contract requires a fully complete design before bidding. Incomplete drawings inflate bids.

- Cost-plus contracts are best suited for complex, fast-track, or renovation projects where the full scope is unknown upfront.

- Item rate contracts are fair to both parties because payment is based on actual work done, not estimates.

- Hybrid contracts are possible. You can combine a lump sum for defined sections and a cost-plus approach for high-risk sections in the same project.

What is a Construction Contract and Why Does the Type Matter?

A construction contract is a written agreement between a project owner and a contractor. It defines the work to be done, how much it costs, and who is responsible when things go wrong.

The contract type you choose decides three things:

- How the contractor gets paid

- Who absorbs extra costs if the project goes over budget

- How easy or hard it is to make changes during construction

Think of it like a restaurant menu. A set meal (lump sum) gives you one price for everything. An à la carte menu (item rate) charges per dish. Room service (cost plus) charges for whatever you order, plus a service fee on top. Same restaurant. Very different bills.

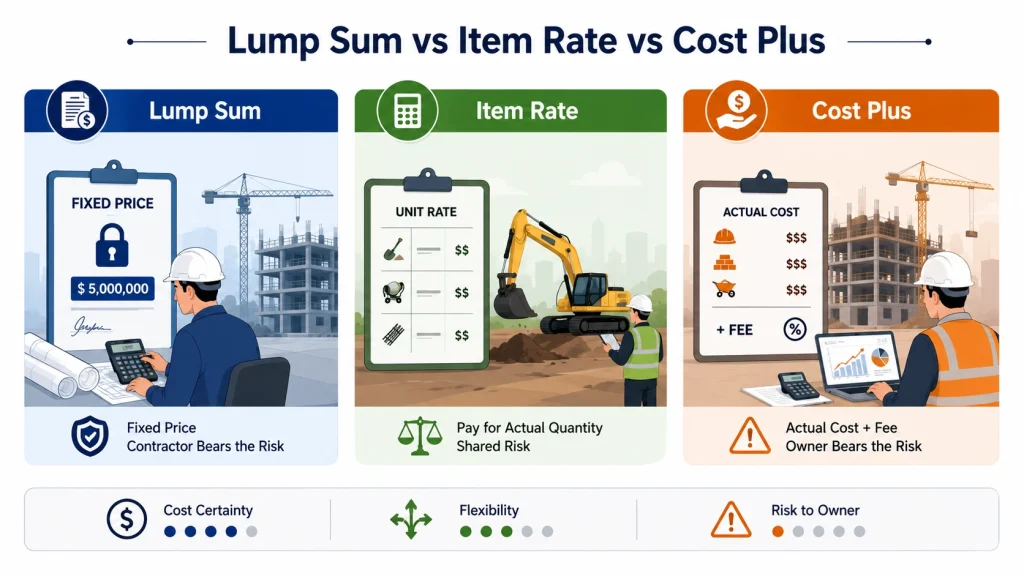

What is a Lump Sum Contract?

A lump sum contract is the simplest of the three. The contractor reviews the full project drawings and specifications. They calculate all costs for labour, materials, equipment, and profit. Then they give the owner one fixed total price for the complete job.

The owner pays that price. Full stop. It does not matter what the contractor actually spends.

How payment works: Payments are made in stages tied to milestones. For example, 20% when the foundation is done, and another 20% when the structure is up. The total always equals the agreed lump sum.

A simple example: A developer wants to build a warehouse. The contractor quotes $5 million. The developer agrees. Halfway through, material prices rise, and the contractor ends up spending $5.4 million. The developer still pays only $5 million. The contractor absorbs the $400,000 difference. That is the core principle. The contractor carries the financial risk.

Advantages:

- The owner knows the full cost before work begins. No surprises.

- Less paperwork for the owner during construction.

- The contractor works efficiently because every dollar saved is extra profit.

- Banks and lenders prefer this contract type because the total cost is clear up front.

Disadvantages:

- Design must be fully complete before bidding. Incomplete drawings lead to inflated bids.

- Every design change needs a formal change order and price negotiation.

- No financial transparency. The owner does not see how the money is spent.

- Vague drawings push contractors to add a risk buffer to their bids. You end up paying for uncertainty that may never happen.

When to use it: Use a lump sum contract when the design is complete, site conditions are well understood, and the owner wants a fixed budget with minimal day-to-day financial involvement.

What is an Item Rate Contract?

An item rate contract (also called a unit price contract) works differently. Instead of one total price, the contractor quotes a fixed rate for each work item. Payment is then based on the actual measured quantities of each item completed on site.

It is like paying for a road trip by the kilometre instead of a flat fee for the whole journey. If the journey ends up longer, you pay more. If shorter, you pay less.

How payment works: The project uses a Bill of Quantities (BOQ), a detailed list of every work item with estimated quantities. The contractor fills in a rate for each item covering materials, labour, tools, overhead, and profit. The formula is simple:

Quantity measured on site x Agreed unit rate = Payment due

Payments are made monthly based on site measurements by a quantity surveyor.

A simple example: A government agency builds a road. The BOQ lists earthwork excavation at $18 per cubic metre. The estimate was 5,000 cubic metres. But site conditions require 6,200 cubic metres. The contractor is paid for all 6,200 cubic metres at $18. The rate stays fixed. Only the quantity changes. The owner pays for actual work done, not the original estimate.

Advantages:

- Fair to both parties. The contractor is paid for what they actually do.

- Quantity variations do not require full contract renegotiation.

- Construction can begin before all detailed drawings are ready.

- The BOQ gives both parties good visibility into where costs are building up.

Disadvantages:

- The final cost is unknown until the project is finished. Budget management is harder.

- Accurate site measurements are essential. This adds admin work and requires a skilled quantity surveyor.

- If BOQ estimates are significantly wrong, the owner faces a much higher final cost.

- Disputes arise when parties disagree on how to measure a particular work item.

When to use it: Use an item rate contract for civil works like roads, bridges, drainage, and earthworks where quantities cannot be confirmed precisely before construction starts. It is also the standard contract type for most government and public sector infrastructure projects.

What is a Cost Plus Contract?

A cost-plus contract is the most transparent of the three. The owner pays the contractor for all actual costs incurred during the project, plus an additional fee covering overhead and profit.

Think of it like hiring a personal chef. You pay for all the ingredients they buy. You also pay them a cooking fee on top. You see every expense. But you carry the risk if ingredient prices rise.

The three main variations:

- Cost plus percentage fee: The fee is a percentage of actual costs. For example, costs plus 12%. The more the project costs, the larger the fee. This can reduce the contractor’s incentive to keep costs down.

- Cost plus fixed fee: The fee is a fixed dollar amount regardless of actual costs. The contractor has more reason to work efficiently because their fee does not grow if costs rise.

- Cost plus with a Guaranteed Maximum Price (GMP): Adds a cost ceiling. The owner pays actual costs plus a fee up to a cap. Costs above the cap become the contractor’s responsibility. Savings below the cap are often shared between both parties.

A simple example: An owner hires a contractor on a cost-plus fixed fee basis. The agreed fee is $380,000. Actual project costs come to $4.2 million. The owner pays $4.58 million in total. If the contractor manages costs better and brings the total to $3.9 million, the owner pays $4.28 million. The fee stays fixed at $380,000 either way.

Advantages:

- Work can start while the design is still in progress.

- The owner sees every cost because all expenses are documented and submitted for approval.

- Scope changes are easy to handle without complicated negotiations.

- Contractors use better materials because they are not cutting corners to protect a fixed margin.

Disadvantages:

- The owner carries most of the financial risk. Cost overruns land on the owner.

- Cost plus percentage arrangements can reward inefficiency. Higher costs mean a bigger fee.

- The owner must actively review costs throughout the project. This takes time and expertise.

- The final project cost is unknown at the start, making financing harder.

When to use it: Use a cost plus contract when the scope is uncertain or still developing, when speed of start is critical, or when the project involves renovation or retrofit work where existing conditions are unpredictable.

Lump Sum vs Item Rate vs Cost Plus: Quick Comparison

Risk: In a lump sum contract, the contractor carries the financial risk. In an item rate contract, the owner carries the quantity risk and the contractor carries the productivity risk. In a cost-plus contract, the owner carries almost all the financial risk.

Cost certainty: A lump sum gives the highest cost certainty. The item rate gives moderate certainty because rates are fixed even if quantities vary. Cost plus gives the least certainty.

Flexibility for changes: Lump sum is the least flexible. Every change needs a formal change order. Item rate is moderately flexible because quantity variations are handled through measurement. Cost plus is the most flexible because scope changes are absorbed into the running cost naturally.

Design stage required before signing: A lump sum needs a fully completed design. The item rate can start once the BOQ is ready. Cost plus can begin with a general scope brief and an incomplete design.

Admin burden on the owner: Lump sum needs the least. Item rate requires regular site measurements. Cost plus requires the most ongoing cost management and invoice review.

How to Choose the Right Contract Type

Choose a lump sum when the design is fully complete, site conditions are well understood, cost certainty is the top priority, and the owner wants minimal day-to-day financial involvement.

Choose item rate when the scope is clear but exact quantities are uncertain, the project involves civil infrastructure, or you are working within a government tendering framework that requires BOQ-based pricing.

Choose cost plus when the scope is uncertain or evolving, the speed of start is critical, the project involves renovation with unpredictable existing conditions, or the owner has the capacity to manage active cost oversight throughout.

Expert Tips for Each Contract Type

Lump sum: Invest in a complete, detailed design before going to tender. Vague drawings push contractors to add unnecessary risk buffers to their bids. Include a clearly written variation clause so any changes during construction can be valued fairly.

Item rate: Use an independent quantity surveyor to prepare and audit the BOQ. The quality of the quantity estimates directly affects how well the final cost tracks the budget. Set clear measurement rules in the contract upfront to avoid disputes later.

Cost plus: Define what counts as a reimbursable cost in precise contractual language before work begins. Set up an invoice approval process with agreed timelines. If budget certainty matters at all, use a GMP clause to cap the owner’s exposure.

Conclusion

Lump sum, item rate, and cost plus contracts are three different tools for the same purpose: managing how money moves on a construction project. Each one fits a different situation.

Read: EPC, EPCM, and Multiple Package Contracts: Differences and Which One Should You Use?

FAQs

What does a lump sum contract mean in construction?

A lump sum contract is a fixed price agreement. The contractor completes the full defined scope of work for one agreed total price, regardless of what they actually spend during the project.

How does an item rate contract work?

The contractor agrees to a fixed rate per unit of each work item. Payment is calculated by multiplying that rate by the actual measured quantity of work completed on site, usually settled monthly.

What is a cost-plus contract in simple terms?

The owner pays the contractor for all real project costs, including labour and materials, plus an additional agreed fee covering overhead and profit, either as a fixed sum or a percentage of costs.

What is the biggest difference between lump sum and item rate contracts?

A lump sum sets one fixed total price for the whole project. An item rate contract fixes the rate per work unit but lets the total payment vary based on actual quantities measured during construction.

Which contract type gives the owner the most cost certainty?

A lump sum contract gives the highest cost certainty. The total price is agreed upon before construction begins and does not change unless the scope officially changes through a formal change order.

Why do government projects commonly use item rate contracts?

Item rate contracts are fair and transparent at the unit rate level. They suit civil works like roads and bridges where exact quantities vary, and they match standard public sector tendering requirements.

What financial risk does the owner face in a cost-plus contract?

The owner reimburses all actual costs. If costs are higher than expected, the owner pays the full difference with no cap, unless a Guaranteed Maximum Price clause is included in the contract.

Can a construction contract mix lump sum and cost-plus elements?

Yes. Hybrid contracts combine both structures. Well-defined work sections use a lump sum price while high-risk or uncertain sections use a cost plus arrangement within the same contract.

What is a GMP clause, and why does it matter?

A Guaranteed Maximum Price clause sets a cost ceiling for the owner. Any costs above that cap become the contractor’s responsibility. Savings below the cap are often shared between both parties.

When should a contractor prefer an item rate contract over a lump sum?

When quantities are uncertain, an item rate contract protects the contractor. Payment is based on actual work measured on site, so the contractor is not penalised for quantity increases beyond the original BOQ estimate.